What are mortgage trusts?

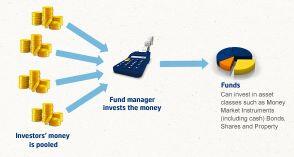

Mortgage trusts are unit trust investments where your money is pooled with that of other investors.

The money is then invested by the manager of the trust in a range of mortgages in the expectation that they can generate an income for their investors at a lower level of investment risk than if they undertook a similar investment individually.

How do mortgage trusts make money for investors?

The money is invested by lending to other parties, usually for the purpose of purchasing existing property. Some mortgage trusts will lend to people undertaking property development. Where development loans are available it is generally expected that a higher level of risk will be experienced (and accordingly a higher rate of return could be expected).

The loan is secured by means of a mortgage over the property. This means that should the borrower be unable to make the agreed payments on the loan, the mortgage trust (as mortgagee) may take possession of the property. The property is then generally sold in order to recover the amount owing to the trust.

Note that:

a) the actual income return from mortgage trusts will vary depending on how the loans are handled by the manager of the trust. (Some managers lend to high risk borrowers and some lend at fixed interest rates rather than variable rates.); and

b) the rate of return is also affected by the amount of cash in the trust. A high cash level generally lowers the income return of the trust but also lowers its risk profile.

Why invest in a mortgage trust?

1. Distributions are often more frequent than other managed investment trusts. A mortgage trust is an income producing investment that is not expected to produce capital growth for investors. The manager of the trust receives the mortgage payments from borrowers and passes them on to you as income distributions, after payment of any fees and charges associated with running the trust.

2. Mortgage trusts are expected to produce income returns higher than cash and term deposit investments. This is because of the higher interest rates usually charged for lending to purchase property, but also reflecting that the investor has undertaken a higher risk than a cash investor leaving their funds in a bank account.

Is a mortgage trust a safe investment?

Mortgage trusts lend for the purpose of acquiring property. There is an element of risk in doing this because the borrower may be unable to repay the interest, the amount borrowed or both. To ensure that the value of the property will at least cover the amount of the loan, most mortgage trusts lend no more than an agreed percentage of the value of the property. Between 66 per cent and 75 per cent is a common, conservative range of lending – this is called the ‘loan-to-valuation ratio’ (LVR) – and before undertaking investment in such a structure, the Product Disclosure Statement (and any subsequent reports on the operation of the trust, should be read with a view to ensuring that the LVR is at a level acceptable to your investor risk profile).

Some mortgage trusts provide a capital guarantee from the manager so that you are guaranteed not to lose any of your invested capital. However, you must be sure the manager is capable of financially meeting the guarantee should it be necessary.

Mortgage trusts also generally allow you to cash in your investment at short notice, say one to two weeks. However, there is a degree of illiquidity in the assets of a mortgage trust as the funds are tied up in loans. Therefore there is a risk when you invest in a mortgage trust that you may not be able to withdraw your funds whenever you want to.

What should I look for in a mortgage trust?

When considering investing in a mortgage trust it is essential you choose one which is offered by a major financial institution with a sound reputation for managing a portfolio of mortgages.

You also need to look at the way in which the trust is managed. Some managers take more risks than others. While higher risk sometimes means higher returns, it also means there is a greater chance of losing some or all of your money.

It is better to be conservative when selecting mortgage trusts and not necessarily go for the one with the highest returns.

Mortgage trusts also vary in the frequency of income payments. Most of them pay income quarterly but some also offer a monthly payment option. This can be helpful in managing the cash flow you receive from your investment portfolio.

Because mortgage trusts are a complex and ever-changing investment it is essential that your selection be backed by on-going research to ensure that it continues to meet your expectations and requirements.

Continuum Financial Planners can help…

The selection and use of specific category trusts within your portfolio is a function of asset allocation. The experienced advisers at Continuum Financial Planners Pty Ltd are backed by processes and procedures to help you make appropriate investment choices: call our office on 07-34213456, or use our website contact us facility to arrange a discussion with one of our advisers about this matter now: –

‘we listen, we understand; and we have solutions’ that we deliver through personalised, professional wealth management advice.

We acknowledge the resources of Securitor Financial Group Limited in drafting the majority of the detail in the above article: it has been extracted from the Support Information to advice documents.

(Originally posted in January 2010, this article has been occasionally refreshed or updated, most recently in January, 2019.)</em