Economic and Markets Outlook for 2018 – a ContinuumFP, in-house opinion

Following our practice over a number of years now, our Economic and Markets Outlook 2018 is presented so that clients, prospective clients and our readers generally are aware of the expectations that our Investment Committee has for the calendar year that has recently commenced. Our discussions with fund manager representatives; and our reading of the reports issued by fund management companies with whom our clients funds are invested (or will, potentially be invested), will be with a view to comparing their investment philosophy with these expectations.

By way of an overview of the expectations for 2018, we are of the view that the respective investment markets will perform similarly to what they did during 2017, albeit with the increasing possibility that there will be a period/ periods of correction1 during the year. Particularly in terms of a diversified, global equities portfolio, any such corrections should present ‘buying opportunities’2.

Economic Outlook 2018

Globally

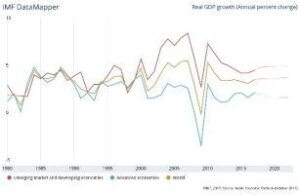

For the first time in a number of years, there is an expectation that growth will be experienced almost universally: whilst rates of growth will differ between countries, regions and development status, the global projection is for growth in excess of 3% for 2018. From an economic standpoint, this heralds well for different economies in different ways. Resource-rich economies will benefit according to the level of increased demand for the resources in which they are rich – but all should benefit to one degree or another.

Services and technology oriented economies will benefit from the increasing demand for improved productivity – and unemployment in most economies should continue to fall (and gradually, wages should increase). Regrettably, this period of increasing economic well-being is also expected to give rise to further geopolitical disruption as the wealth gap continues to grow.

Inflation is not expected to pick up any time soon, in spite of the roles – and endeavours – of Central Banks in that regard.

The USA

In spite of popular opinion as to their President, the US economy is expected to continue to grow at an eye-watering 3+%, with unemployment now being tipped to fall to the low 3% range – with an increased labour market participation rate.

The increasing independence in fuel oil/ resources production is rapidly improving their economy, with less wealth being focused on security of supply; and more into productive enterprise. Both manufacturing and the services sectors are expected to continue to improve during 2018.

The tax cut legislation will be felt as from early February 2018, increasingly through a twelve-month cycle, all the while increasing consumer confidence (as well as the confidence of business operators, small and large). As a consumer-driven economy, this bodes well for the US economy – and as the global economic powerhouse, that will also help fuel the global economies that trade with the USA.

The Fed (The Federal Reserve Bank of the USA) is expected to raise the official interest rates three or four times during 2018 – each time by 25 basis points; and they are also expected to reduce their Balance Sheet (Bond-buying) at a continuing steady rate. These are tightening measures, but at a very measured pace: the expectation being that whilst the Balance Sheet reduction will carry on regardless, if there are any concerns, the continuing rate of rate hikes may slow.

China

As a controlled economy, China has both intrigued capitalists with its phenomenal growth over the past decade or so; and raised the scepticism levels as to the truth of its reported economic growth. With growth projections now back around the 6% mark, most commentators are more comfortable with the reports; and most are satisfied that the forecasts by the Chinese Central government, are probably credible.

The Chinese government’s control over the property market has been fruitful in preventing a residential property bubble; and the main concern on the economic horizon for China, is the debt management issue that they will need to show leadership over, during the coming two years.

Europe

As an economic block, Europe is a conglomerate of 27 independent nations and whilst there is free trade across borders in that block, they trade outside the block as a single economy. The European Central Bank has been careful in selecting policies from the experiences of their American counterparts and seems content to trail behind the USA in the growth of their economy and the management of their constituents’ expectations. Further easing is anticipated, but at a slower rate during the year, perhaps ceasing early in 2019.

There are a number of elections happening in the Eurozone during 2018 and there is some anticipation of civil unrest in some areas, including in Spain, Italy and (though more remotely likely) in Greece and Germany.

Emerging Market economies

Traditionally – and continuing so – there are risks in emerging market economies that include political instability, absence of financial controls and corruption concerns; and whilst these are not all present in all emerging economies, they result in lower valuations and higher expectations of risk. Nevertheless, the expected universal tide of growth is expected to ‘raise these boats’ as well.

Economies in this group include some of the Central and Southern American countries, a number of Eastern European and Asian countries and a few of the African countries. Typically, they are resource-rich, low-cost labour economies with ambition to become wealthy nations – and they will contribute to global growth as demand for those resources increases.

Australia

The Reserve Bank of Australia (the RBA) is closely monitoring all of the economic factors in the Australian economy, but seems content with the pace of developments for the present time. They are not expected to raise official rates again until 2019, unless some significant change happens in the meantime.

Our rate of unemployment is falling as new jobs are being created; wage growth has been stifled, but work participation is improving: personal debt is an area of concern and pressure by regulators has curtailed some of the easy lending practices that existed up until only several months ago. With commodity prices falling, but the exchange rate for our currency compared to the basket of our trading partner currencies, suggests there will be continued high demand for our exported goods – commodities, farm produce, financial services and to a diminishing degree, manufactured goods.

As per the following Table, the RBA expects the Australian economy to grow by around 3% for 2018.

Markets Outlook 2018

Equities

Whilst there has been a lot written about the ever-increasing valuation of equities, particularly those of the USA, the ‘lower returns for longer’ mantra seems to support the current and projected valuations, particularly as profitability increases, the low interest environment persists – and for some, lower tax costs are imposed.

A common measure of where the equity market valuations sit, is the PE3 factor: currently in the USA, this factor is about 20% above the long-term average. At around 17 times, against a long-term average of just over 13 times, the profitability of the companies making up the publicly-traded market sustains this valuation, yielding higher returns than do Cash and some Fixed Interest products.

The PE factor for most developed economy markets is similarly above their long-term averages. However, the emerging market economies, whilst relatively highly valued at the present time, are only trading at around the long-term average.

Being conscious of the fact that the sharemarket is traditionally, a forecaster of economic conditions ahead; and believing that the sharemarket will continue to rise during 2018 (even allowing for the possibility of corrections in some of the equity markets), the lack of any forecast of a recession on the economic front supports the positive outlook for equities globally for 2018.

When considering equities in a region by region context, it is expected that the rising tide will lift all boats: the PE valuation basis for emerging market equities probably makes them marginally more attractive than the broader market place, but the risk factors need to be taken into account by individual investors.

Fixed Income (Bonds)

The Fixed Income market is broken down into a number of components: government bonds, corporate bonds, high yield bonds, hybrid securities and others – each has its own characteristics, different risk factors and different return characteristics. Each of the types of security that make up this market can be issued by ‘entities’ in developed, emerging or frontier economies – and within each of those markets, these securities will be assigned a risk rating (both by ratings houses and the market participants – or investors).

As with most traditional markets, returns from Fixed Income products either come from trading activity, or coupon realisation. In a market where there are low returns offered for holding the bond; or there is a risk that the coupon yield will be diminished as new, higher interest-bearing bonds issue, trading bonds is popular: where there is price stability (low volatility) and little expectation of interest rate rises, the return from realising the coupon are more attractive. In the first instance, a shorter duration portfolio is favoured whilst in the latter scenario, a longer duration portfolio will likely result.

In the economic and market environment we have forecast for 2018, we believe that a longer-duration traditional bond portfolio will serve the investor well.

Property (Trusts)

This asset class has seen a significant resurgence since the GFC of 2008: but regional and economic factors are limiting its future growth. Traditional bricks and mortar retail outlets are diminishing in importance, factories are becoming mega-sized; and work patterns are changing in many occupations. Residential accommodation in the large economies of the USA, China and others appears to have reached a ‘peak’ (particularly in China), as it has in Australia: nevertheless, low interest rates suggest that the current valuations are sustainable (no doubt with some regional variations).

Investment Strategy

Individually, investors need to be aware of their investment risk tolerance rating, and to be aware of their (attainable) investment goals and objectives; and in the context of the outlook for 2018, we suggest that the following elements will be part of a well-managed portfolio –

- Long-term, yield-bearing assets

- Diversified over asset classes – and regions

- Fully invested (to suit individuals’ circumstances); and

- Regularly reviewed (against SMART4 investment goals);

…and we will be looking to our investment managers to underpin these characteristics in the way they manage the funds entrusted to them on behalf of our advised clients.

Investment advice in the context of your economic and markets outlook 2018

Whether you are investing for near-term or longer-term goals; and whether your investments are within a superannuation/ pension environment, or outside of that structure, the experienced advisers at Continuum Financial Planners Pty Ltd are available to provide you the appropriate advice to guide you towards the best outcome, in your best interests – and at fair value. This economic and markets outlook 2018, shows the basis on which our investment philosophy for 2018 will be formed, at least during the first half of the year. To experience our mantra, that ‘We listen, we understand; and we have solutions’, call our office (on 07-34213456) to arrange a meeting with one of our advisers; or you can complete the Contact Us form.

For other views on economic and markets outlook for 2018, you could look to the websites of MoneySmart, the Reserve Bank of Australia (the RBA) and some of Australia’s large Banks (including Macquarie).