Introduction

Our view of the economic and markets outlook for 2020 provides a background to the expectations we have for the 2020 calendar year and it will be reflected in the way we review and assess investment assets for retention in, or addition to, client portfolios – at least in the early phases of the year.

This article expresses an opinion only, and any opinion/ quantification expressed should not be treated so much a forecast, as an estimate. Any comments in this article are to be considered general in nature and should not be acted upon without seeking the advice of a professional wealth management adviser.

Our expectation of the economic and markets outlook 2020, is expressed below: it has been compiled from our experiences during recent years, our awareness of the economic conditions that are reported for key economies – and our understanding of the risks to the orderly conduct of markets as revealed by current affairs reports and the opinions of economists and analysts employed by, or consulting to, a range of Fund Managers. (Credit is given at the end of this article, to the particular groups/ entities that we have relied upon in the formulation of this outlook.)

The ContinuumFP response to our economic and market outlook for 2020

The processes we engage in the selection of investment managers in whom we put trust to best manage our client investment portfolios to optimise the outcomes from the economic and markets outlook, include –

- the research and strategy development process adopted by the manager (which in a multi-manager case includes their process of selection and ongoing evaluation of, managers with whom to invest into particular asset classes);

- the sustainability of their operations (how long have they been providing the service offered; how stable is their team; how open they are in communicating their strategy – and in reporting their outcomes, favourable or otherwise);

- the performance history they have achieved, with an eye as to its consistency (indicating the effectiveness of their strategies and processes);

- how ‘true to label’ they are in terms of consistent application of their strategy and process to investments; and, because not all client needs are the same,

- how relevant the above aspects of the manager are to the financial goals, objectives and risk profile of our clients (on an individual basis).

Other factors are also taken into account, but the ones detailed above are those that go to the likely performance outcome – and they are the ones that will take into account all of the likely headwinds and tailwinds in a professionally conservative way that gives us confidence that our clients funds will be managed so as to take advantage of opportunities relevant to their investment objectives and investor risk profile, whilst minimising the effect of any negative market event on their capital.

Economic and Markets Outlook 2020

Our view in summary:

The helicopter view of the year is that globally from an economic viewpoint, developed economies will perform a little better for 2020 than they experienced in 2019; the US – which had a stellar 2019 – is expected to perform well, but not to eclipse that year in 2020; and emerging economies are likely to perform with inconsistent results, but a number of them, considerably better than they did in 2019 (significantly because they are coming off ‘a low base’). From a markets viewpoint, we expect that the US equities and bond markets overall will generate medium-range, single digit returns of between 4% and 6% (in their local currency); and global markets performance outside the US are expected to generate returns in a slightly higher range of between 6% and 9%. Overall, a moderately conservative diversified portfolio might reasonably expect a return for 2020 in the vicinity of 7%.

Factors to consider

As is always the case, any expression of economic and markets outlook is largely speculative. We caution readers to be aware that factors can develop and impact markets, whilst sometimes anticipated, rarely with timing and consequence certainty, without the knowledge or prior awareness of all participants. Some of the factors that we are mindful of and are alert to throughout the economic cycle, include –

- geopolitical/ political events;

- natural events (disastrous or otherwise);

- technological developments;

- consumer sentiment; and

- demographics

(We acknowledge that some readers may categorise other events, or categorise some of the above events differently, from our consideration of them, but these are the main ones we believe are likely to provide head- or tail-winds to economic and market performance for 2020.)

In October 2019, the IMF projected global economic growth for 2020 to be 3.4%, but cautioned that instability in some emerging markets and slowdowns in China and the United States could subdue this outcome to be little better than the 2019 actual performance (the details of which are yet to be determined). They called for policy makers to take decisive fiscal action to bolster their economies – and for China and the US to focus on easing the trade tensions created by their ‘tit for tat’ approach to bans and tariffs.

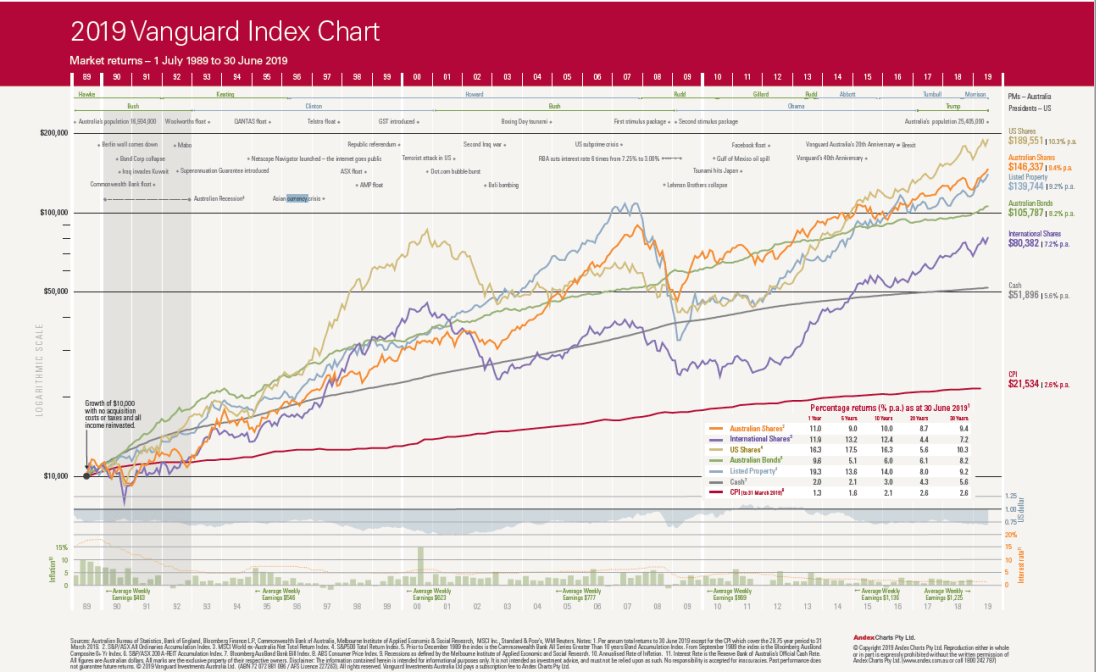

Click on image for larger, clearer view of the Vanguard Index Chart of market performance from 1989 through 2019.

Geopolitical/ political events

Each year we encounter new political events that are credited with disrupting the orderly progression of investment markets on their presumed ‘inevitable’ ascendance: the fact is that these are all part of the social fabric in which economies exist, investors live, and in which markets operate. We perceive these events more likely to provide support for the markets during 2020, than ultimate detraction – but acknowledge that there will be periods of volatility to navigate.

The key events from a geopolitical scenario (those where there are cross-border consequences), are those that impact on the normal course of business, or on the normal flow of ‘trade’ between economies. In this context, the trade tension between China and the US has been the elephant in the room for the past year; vying closely behind has been the Brexit saga between the UK and Europe; tariff threats by the US on a number of its trading partners (think Europe, Australia, and near neighbours and allies of the US!); instability in the Middle East (where Iran, Turkey, the Lebanon, Syria and Israel are struggling to find a way to co-exist, or to even seriously consider a way to do so).

At the political level, political parties in a number of the world’s developed economies are struggling to form majority governments. The consequences include paralysis of decision-making by governments at a time when most economists and analysts – including those at the IMF – are calling for them to take decisive fiscal action to stimulate their economies.

Elections are scheduled around the world again this calendar year, in Europe, parts of Africa, and in the USA, where the President, Donald Trump, is seeking a second term in office.

Economies become beholden to business in the turmoil arising from these circumstances – and business, particularly ‘big business’ such as multi-national corporations – can adapt to the regulatory and fiscal environments that are available to them, continuing their progress in spite of government inertia. Governments are perceived by some commentators, to have yielded their control of economic resources to business: and, correctly or otherwise, this has led to the perception that business gouges the economies for the benefit of the few (their shareholders and senior management).

As intimated above, the timing, duration and extent of consequence of any political/ geopolitical events is unpredictable. From a market point of view, this outlook means that in the absence of political (policy/ regulatory) stimulatory influence, the outlook for market performance for 2020 as expressed above, is feasible, albeit that the route to the eventual outcome may be volatile.

Natural events

Natural events can have extreme effects on economic and market performance, either beneficially through timely weather events such as ‘normal’ rains, sunshine and breezes; or disastrously through excessive rains (and flooding), snow, winds (and cyclones/ tornadoes etc) or drought – and in the face of current events here in Australia, we can add to that list, bushfires.

Without ignoring the possibility that recent climate changes are as a consequence of mankind’s abuse of the fragile environment in which we all operate, these natural events appear to be becoming more extreme, less predictable and more difficult to manage or control.

Primary production, which is the source of the food we all need to consume, becomes less predictable, as to timing of product available for the market, the quality of that product and the cost of the product to the consumer. These consequences impact directly on the economy and on the markets.

Investors like consumers, are at the mercy of the weather patterns – and of the adaptability of the farmers to harness evolving environmental conditions to produce good quality produce, in sufficient quantities and on a reliable basis to sustain the needs of consumers; and to sustain a reliable market.

Improvements in transport technology, and in the speed and cost of transport around the world, provides some assurance that the consequences of extreme natural events should be short-lived. They should not have any lasting impact on the economic and market performances suggested earlier in this article. Again, the nature of these influences is such that neither timing, duration, nor the depth of effect can be predicted.

Technological developments

Technology is impacting our lives at a seemingly increasing pace over time. Technology in this context, refers to electronics, computers, the internet of things (IOT), big data, artificial intelligence, virtual reality, robots, autonomous vehicles, the cloud and like developments.

The efficiencies that technology brings, albeit accompanied with the fear of displacement from the workforce, mean that some activities that couldn’t be undertaken (or even envisaged) in the past are now becoming commonplace – and in many cases, affordable. This efficiency requires investment – and for the most part, increases workforce productivity.

People born during the first couple of decades of the twentieth century, saw the rapid rise of the automotive industry, advancements in the development of aeroplanes (that eventually facilitated affordable travel over lengthy distances), and changes in how society chose to live – moving further into urban environments and away from rural communities. Those changes were no doubt, challenges to the people themselves, to the governments that had the responsibility to regulate those developments – and to investors who struggled to ‘pick winners’ in the enterprises that facilitated many of these developments.

The current crop of post-millennials (or Gen Z), born during the first twenty years of this century, don’t understand the concept of putting money into a phone box to initiate a call to a friend – and are bemused by parents and adults who question their insatiable use of mobile smart devices from which they can make phone calls (though rarely do), send messages, manage their bank accounts, watch streamed video productions, compete in electronic games with others (who could be on the other side of the world), whilst checking the weather forecast, ‘googling’ any question they have…and so on. They are also likely to go through life without either having a driver license or owning a motor vehicle: they will also be enjoying virtual experiences sitting in their parent’s loungeroom as realistic as their forebears had at great cost (and in some instances, considerable risk), travelling abroad.

The point of all of this, is that while times are changing this is not a new experience for us as consumers, or as investors. The rate of change may appear to be increasing but the capacity to cope with the changes endures. We expect that the effects of technological developments on the economic and markets outlook for 2020 will be beneficial and supportive of the anticipated outcome expressed above.

Consumer sentiment

This is a very fickle area of consideration: consumer sentiment often stays within a trend range for reasonable periods of time – however, the sentiment reading for consumers in any economy around the world is often quite different from that concurrently registered in most other economies – either from a trend directional viewpoint, or as to the positive or negative positioning.

For 2020, there is reason to believe that consumer confidence will be positive in North America, Western Europe, and in parts of Asia. On similar reckoning, it is expected that consumer sentiment will be neutral in other parts of Asia (including Australia), in Eastern Europe and in parts of Africa. Negative consumer sentiment is anticipated in other parts of Africa, South America and in the Middle East.

Given that most Western economies – particularly those that are labelled the developed economies – the consumer is the greatest contributor to the economic prosperity (the GDP) of their countries, investors need to remain focused on how their funds are allocated to take advantage of opportunities arising from changes in this particular metric. Because it is usually such a slow-moving metric – and one that can be quite erratic – short-term decisions should not be made on this element alone.

The managers of investment funds will rely on their analysts interpretation of this measure when considering tactics to optimise the returns on their clients’ money, but there is little expectation that consumer sentiment alone will have any significant impact on the economic and market performance likely to be experienced for 2020, as expressed earlier in this article.

Demographics

For more than a decade now, researchers have been alerting governments and corporations as to the impact of the ageing of the populations of developed economies. The impact is of interest because it means that the previous model of taxation and social security for the aged will be challenged by the ratio of income-earning workers contributing tax (from which social security services are funded) diminishes relative to the numbers in their population who are dependent on that support.

Governments are adopting a range of measures to address this issue: they include –

- incentives to young people to have (more) children;

- accepting more immigrants with targeted skills; and

- encouraging older workers to stay actively employed/ engaged.

One of the effects of the growing imbalance between working members of the economy and the aged needing their support, exacerbated by the technological changes we are undergoing, has been that the millennials are becoming the first generation in over ninety years, to have the prospect of a future that is less financially certain than was that of the previous generation.

There are financial consequences of this for both economies and for markets. In formulating this economic and markets outlook for 2020, we accept that the awareness of this situation has been taken to account in calculating the likely outcomes for the year. Indeed, we believe that the returns expectations would be for higher if satisfactory solutions to this dilemma could be found.

Harking back to the commentary above regarding technological developments, there is a sense that the millennials and post-millennial generations are going to have to be educated with different skills and undertake activities differently than have earlier generations. (Some readers might observe that this has been the case since the start of the Industrial Revolution a couple of centuries ago!) The focus on STEM subjects in education systems around the world is a start to that process. (STEM by the way, is Science, Technology, Engineering and Mathematics.)

Those economies who gain an edge in the development of their populations in these specialist areas will gain ‘first mover’ advantage over other economies and investment analysts and economists will be keen to identify them – and corporations operating in those economies – as investment targets for future growth.

Constructive, thoughtful comments in relation to any of the views expressed herein are welcomed and, after mediation will be published on this site.

The team at

Continuum Financial Planners Pty Ltd

Continuum Financial Planners Pty Ltd adviser team is at your service.

If the economic and markets outlook 2020 is something that you need to take into account in managing your investment portfolio – or in planning to start that wealth accumulation process – contact our office to be connected to one of our qualified, experienced advisers. We can be contacted by phone to our office (07-3421 3456); or by completing and submitting the Contact Us form on our website.

Details of the services we offer, how we provide them – and answers to questions about financial planning, can be found in the linked areas of our website: you are invited to explore them before committing to meeting with us.

Information sources researched in the formation of the opinions expressed in this article are as follows: (If you would like to read the articles from these sources, please contact us for a copy of the relevant link.)

Barrons (December 2019) – see stock (equity) valuations as challenging and project a 4% growth on the S&P 500 in New York during 2020 and suggest that a dividend yield of 2% during that year will deliver the 6% growth forecast by a range of strategists they consulted.

Franklin Templeton (December 2019) – over a range of articles, this group has shunned the prospect of any recession (either in the US, or globally) during 2020 and suggest that cautious investing should return positive outcomes for the year, with opportunities in both equities and bonds.

JP Morgan Asset Management (December 2019) – favour equities over bonds for 2020, seeing growth in equity values globally (though at a higher pace external to the US, than within that market). They caution as to periods of volatility and suggest being ready to seize on opportunities those periods present – including, in well-researched emerging markets.

Macquarie (December 2019) – foresee oscillation between optimism and pessimism during 2020, with equity and bond markets likely to continue their positive trend throughout the year, but indicating that not all investments will rise in unison (‘a rising tide will not lift all boats equally’).

Morgan Stanley (December 2019) – who addressed the economic growth forecast, projecting global growth for 2020 on a Q4/Q4 basis of 3.5%, with the US only being credited with 1.8% on that same time basis.

Russell Investments – expressed a positive outlook for equities globally for 2020, but some reservations about the performance of the bond market (indicating that credit looks expensive for 2020). On a currency basis, they favoured the Japanese yen; and perceive the pound sterling as undervalued going into 2020.

IMF (October 2019) – raised their projection for 2020 (from the forecast made in April 2019), to 3.4% for the year.

PIMCO (September 2019) – who have a conservatively positive outlook for the global economy, but caution that lower performance levels will persist as will volatility: they suggest caution, but taking action when opportunities present.