Dollar cost averaging proves that ‘Slowly but Surely may well Win the race’

Dollar cost averaging has proven itself effective in the continuum of market cycles, regularly demonstrating that investment success comes with patience: but what is it? – and why does it work?

What is it?

Dollar cost averaging (a tried and tested financial wealth management strategy) is a process of investing a similar amount at regular intervals into a single portfolio. An example of this is say, $100 per month into a bank passbook account. In this instance you will mainly benefit from ‘the magic of compounding interest’, but when investing into other asset classes such as shares or managed funds investing in fixed interest, shares, property and other growth assets – you will benefit from both the averaging of the purchase price – and the compounding of earnings.

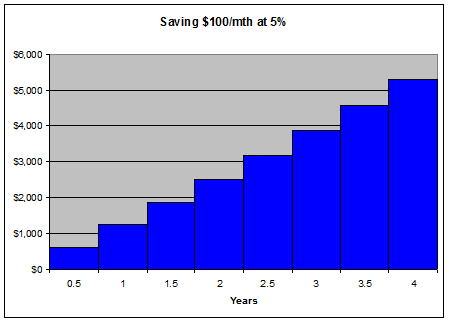

Getting back to the simple example above though, having run the savings program for a few years – say at $100 per month to a passbook account earning 5% per annum1 credited monthly – we accumulate $5,000: now we feel confident to invest some of the saved money. (We may decide to keep a portion for a rainy day – or some opportunities!)

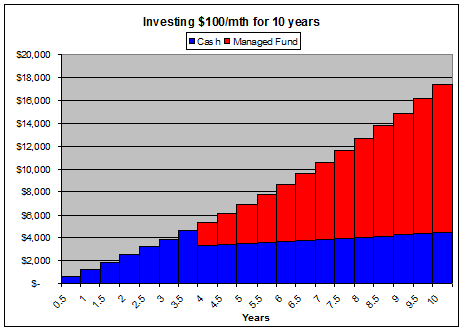

… and so we continue to ‘invest’ $100 per month – but now it is into a diversified, multi-manager managed fund account started with say $2,000 from the original account. (For purposes of the exercise we assume a Balanced Risk Profile and anticipate a 30% tax effective income distribution of 4% p.a., paid quarterly; and capital growth at an annual average of 5% p.a. – although it should be anticipated that in some short periods there could well be negative growth in the accumulated capital.)

Ten years from starting out on this process, we have accumulated $17,380 and have hardly missed the $100 per month, especially as our income from which it is invested has likely increased throughout this period.

Why does it work?

Without running an expose on investment theory, the quick summary of the success of this story is that the investments are made consistently over a range of market conditions, so that whilst some of the funds will be invested at a higher average cost, some will also be invested at low average cost – and the majority will be invested in average market conditions …

BUT the real secret of this success is the consistent investment of an affordable amount throughout a term regardless of other circumstances and situations – that is, we don’t run hot and cold with whether we will invest or not! [There is material available that will show that investors who try to time the market often miss critical days – or times of day – and in doing so, miss significant value. Dollar cost averaging works through all this and brings consistently improved outcomes for the patient investor.]

This strategy can be useful for a number of financial objectives (including some of those in our article ‘Planned investment based on available resources‘; and think about your regular superannuation contributions).

Would you like to experience investment success?

You can experience investment success through a strategy as described above – and members of your family can also benefit even if at a lesser level of commitment. To get started, meet with one of our experienced financial planners (or to refer a family member or friend to have such a meeting) – and enjoy the Continuum Financial Planners experience – ‘we listen, we understand and we have solutions’ – call us on 07 34213456; or use our website Contact Us page.

1 The current bank savings interest rate will depend on the type of account you select – and the market for cash rates at the relevant time. This figure has been selected as a longer-term average and for ease of understanding: the principle is the same regardless of the rate of interest.

[Originally posted in 14 July 2010 under the title ‘Slowly but Surely (may well win the race)’: this article has been occasionally refreshed and updated, most recently in March 2017]